Japan

• The decision statement describes rates as “at significantly low levels,” even as they edge toward the BOJ’s 1% estimate for the lower bound of neutral. That suggests the bank now sees neutral as higher, giving it room to tighten further.

• The BOJ conveyed a clear willingness to keep raising rates. It released an referential note that lay out three drivers behind Friday’s move: reduced uncertainty around the US economy and trade policy, expectations for solid wage gains next year, and a rise in underlying inflation as firms pass on higher labor costs. The message: the BOJ is more confident that its price outlook will be achieved.

[Why the BOJ Hiked on Friday?]

Ueda pointed to a stronger assessment of domestic and global conditions as the backdrop for the move.

- On Japan, he highlighted corporate-profit upgrades in the Tankan and said uncertainty around US tariffs had eased. Ueda said some board members cautioned that higher import prices — driven by the recent yen weakness — could pass through to underlying inflation.

- On the US, Ueda said downside risks had faded, thanks to firm consumer spending and AI-related capex. He added that China’s slowdown is unlikely to tip into a deeper slump due to policy support.

[The Rate Path Ahead]

As we had anticipated, Ueda offered no explicit guidance on the rate path, repeating that decisions will depend on economic and market developments.

• He said the BOJ will assess how the new rate affects the economy, inflation, and lending conditions. That aligns with our view that the next hike will not come quickly — and is unlikely before July.

• That said, we see that he is confident of achieving the central bank’s inflation target in the medium term. He forecasted that headline CPI may dip below 2% next year due to base effects from the food-price surge earlier this year. But he stressed that the impact on underlying inflation would be limited as the wage-price cycle would continue to build.

[The Neutral-Rate Debate]

Ueda fielded numerous questions on the neutral rate. His core message: “We won’t know until we get there.”

• Some markets had anticipated an update to the BOJ’s neutral-rate estimate. But it refrained from it, and Ueda even appeared to have downplayed the importance of statistically derived estimates, indicating that observed economic responses after rate hikes carry greater weight.

• He offered two reasons for keeping the phrase “significantly low” in the statement, both of which have nudged markets toward a higher view of the neutral rate.

o First, he emphasized that 1% is only the lower end. With about a quarter of Bloomberg-surveyed economists putting neutral at 1%, downplaying that level sends a mildly hawkish signal.

o Second, he observed that even after the shift from negative rates, the tightening effect on the economy and financial conditions has been limited. This shows the BOJ is willing to adjust rates according to its assessment of the economy rather than be constrained by neutral-rate estimates.

• It also wouldn’t be a surprise if the board’s views of the neutral rate is drifting higher. Since Ueda broached the 1%–2.5% range in January, inflation expectations have risen. The BOJ also pointed to signs of improving real productivity in the April’s outlook report (Box 2 in the report).

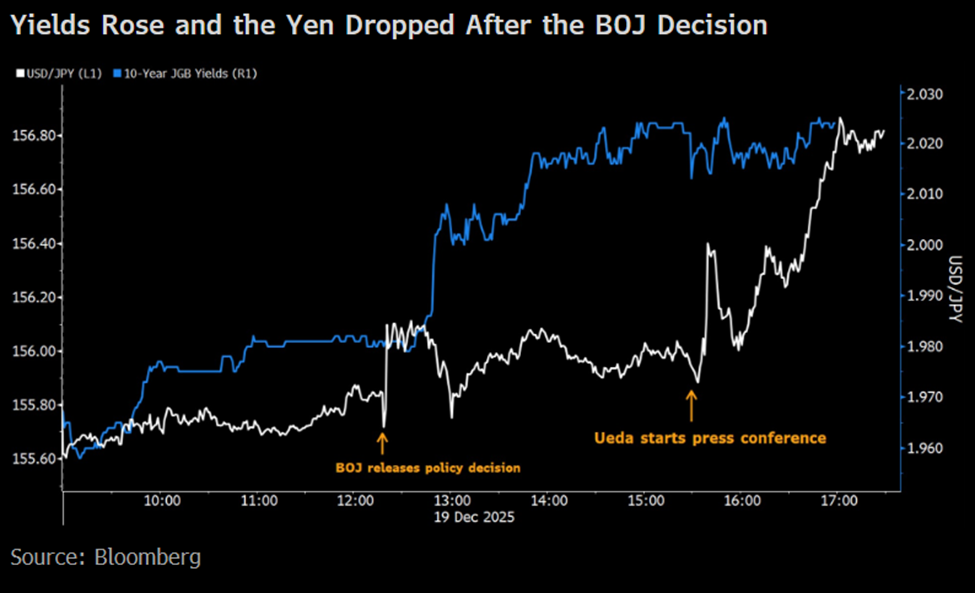

[Market Reaction]

After the policy release, JGB yields rose while the yen weakened against the dollar. The conflicting move likely reflects the markets’ dovish reading of the BOJ’s comments - which they think point to a slow adjustment path of its policy rate and higher inflation expectations.

Looking ahead, that interpretation could flip, in our view. As long as yen weakness and sticky CPI inflation persist at higher than 2% — and coordination with the government remains smooth — the BOJ is likely to proceed with further tightening.

• Ueda stressed at his press conference that the central bank has had close communication with the government. If Takaichi — while seen as reluctant for the BOJ to tighten BOJ — view yen weakness and inflation as political liabilities, she could easily greenlight additional hikes.

'글로벌 매크로' 카테고리의 다른 글

| 2026/02/20 - 일본 금융시장이라 정책변수 (0) | 2026.02.20 |

|---|---|

| 2025/12/20 - December FOMC 25bp rate cut (0) | 2025.12.31 |

| 2025/11/28 - BOK keeps rate steady, possible end of easing cycle (0) | 2025.11.29 |

| 2025/11/20 - Rising possibility for FED Rate Cut and 21 trilltion JPY stimulus package (0) | 2025.11.20 |

| 2025/10/24 - U.S September CPI data release (0) | 2025.10.25 |