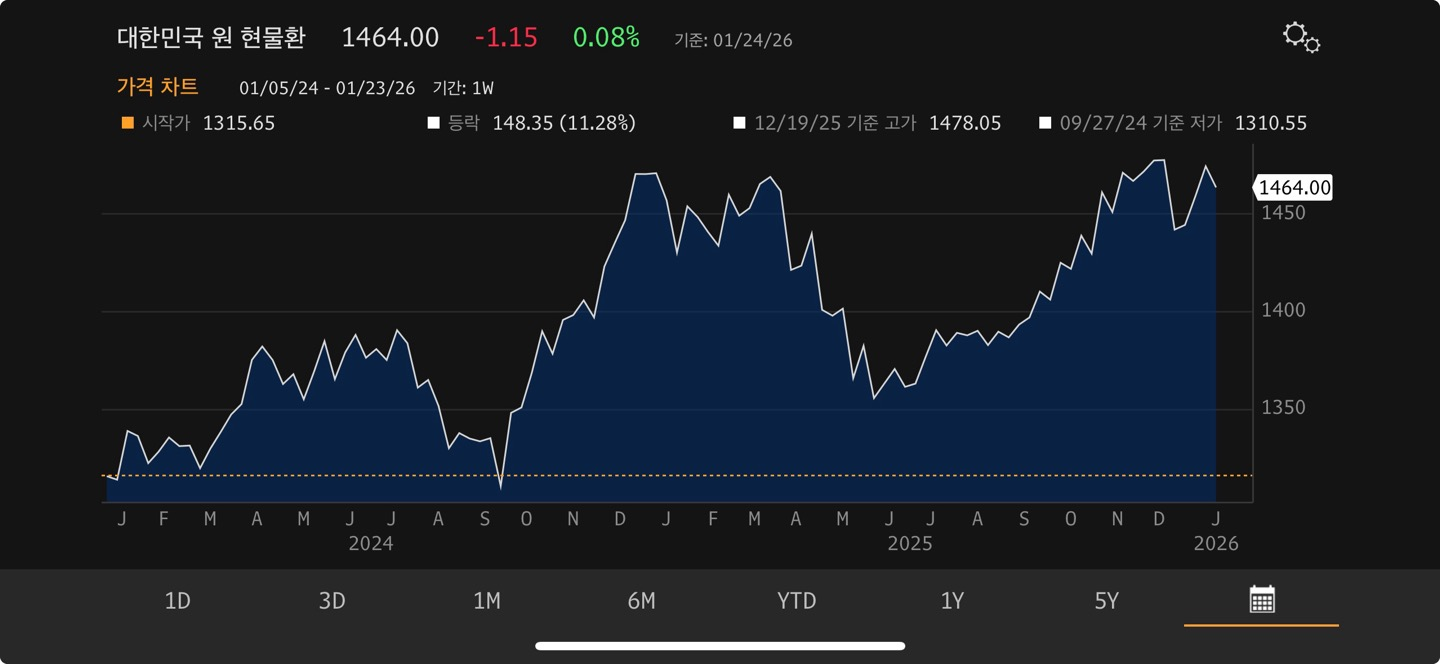

Sharp drop in the USD/KRW exchange rate in 2025 May was suspected to be triggered by Taiwan Life Insurerer's proxy hedge. Taiwan Life insurerers have been actively trading in the USD/KRW market since late 2010s. And when there has been volatility in the KRW market for example at May or Dec. in 2025, they were always involved.

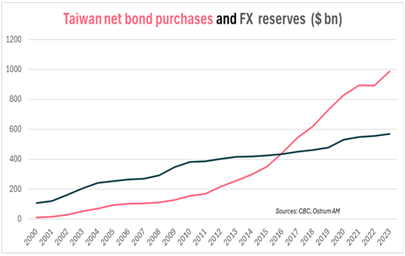

Panic spread through Taiwan, prompting massive sell-off of USD which led to a sudden appreciation of the TWD. Although causes remain unclear, it has highlighted the colossal amount of foreign financial assets accumulated by Taiwan, totalling $1 trillion, which is 200% of its GDP. Life insurance companies hold more than $700 billion, primarily in U.S. bonds (Treasuries and investment-grade corporate bonds). Their hedging needs are met by the Central Bank of China (CBC), which provides them with dollars from its substantial FX reserves through currency swaps.

Over the years, lifers became lax (to become loose, careless, or not strict enough), accumulating risks: $200 billion in foreign bonds are uncovered, representing 25% of Taiwan's GDP. Their solvency relied on a fragile balance, particularly on the belief that the CBC would never allow TWD to appreciate. Life insurers have recorded significant potential losses, which may worsen if U.S. interest rates continue to rise and the greenback weakens.

TWD suddenly appreciated 4% against USD. Massive USD sales by exporting companies aiming to secure their profits amid rumors that the CBC would cease to guarantee the exchange rate of the USD/TWD. Panic also gripped life insurers who massively sold USD out of fear of a currency mismatch between their assets and liabilities.

Since the early 2000s, Taiwan's current account balance rapidly increased, reaching nearly 15% of its GDP in 2014. This led to the accumulation of foreign currencies, notably U.S. dollars, housed in the central bank's foreign exchange reserves. Central Bank of China (CBC) decided to redirect a portion of these reserves to life insurance companies, a significant sector in Taiwan’s economy that represents 60% of its GDP. Massive issuance of “Formosa Bonds” resulted in Taiwan's foreign financial assets reaching $1 trillion, equivalent to 200% of the country's GDP.

The CBC uses a portion of its FX reserves to provide currency financing or hedging to lifers. CBC employs currency swaps: the CBC exchanges foreign currencies for TWD, and the lifers exchange these TWD for foreign currencies, which they then invest abroad.

This mechanism has also helped mitigate fluctuations in its currency on the FX market, particularly by curbing its appreciation against the US dollar. (TWD를 안 사도 되게 해주는 시스템으로 이해함..대만 중앙은행이 계속 쌓여가는 외화 자산을 보험사한테 쉽게 넘기니깐??) Through this swap mechanism, Taiwan's FX reserves have not increased, allowing the country to avoid being classified under "monitoring" by the US Treasury for currency manipulation. However, CBC disclosed its positions in currency derivatives for the first time in 2020.

Taiwanese consumers preferred life insurance policies that pay in local currency rather than in USD. Taiwanese life insurers primarily fund themselves in TWD, even though their investments are increasingly denominated in USD.

- Currency Risk: weak USD would lead to significant losses due to the substantial foreign currency mismatch between assets and liabilities.

- Hedging Cost: primary cost impacting the profitability of life insurance companies. Selling USD forward can protect life insurers from spot rate fluctuations, but maintaining these positions can be costly.

- Interest Rate Risk: rapid increase in U.S. interest rates can lead to significant losses on their bond portfolios.

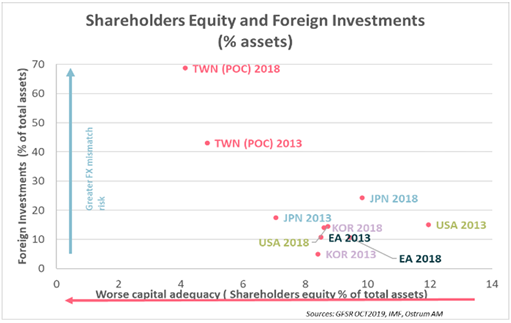

Lifers have hedged their portfolios only partially. Only half of their currency mismatch between assets and liabilities has been hedged. In the event of real losses, lifers can absorb them with their shareholders' equity. However, Taiwanese life insurers are less capitalized than their Japanese counterparts, as demonstrated in the bottom chart.

NDF Market in the contagion to other Asian Currencies

Hedges by NDF are settled in USD abroad, exempting lifers from securing financing in local currency when needed. Taiwan's FX market is narrow, and the regulator prohibits companies and financial institutions in the country from trading TWD in the NDF market. To circumvent this restriction and hedge their foreign currency investments, Taiwanese life insurers use so-called "proxy" currencies like the KRW. The South Korean economy shares similarities with that of Taiwan, as both are heavily dependent on exports focused on similar industries, such as electronic components and semiconductors. Taiwanese life insurers, driven by panic, rushed to cover their uncovered dollar exposures on the NDF market, this led to the sudden appreciation of the KRW. (즉, 헷지하지 않은 달러 자산이 너무 많았기에 헷지하기 위해 TWD, KRW 대량 매수했다는거..?)

sdfasfas

'공부내용' 카테고리의 다른 글

| [FICC] 국고채 바이백, 통안채, 외평채 등등 (0) | 2026.01.12 |

|---|---|

| [매크로] 주요 경제 지표 해설 (0) | 2025.06.30 |

| [매크로] 연방준비제도의 내부구조 그리고 각종 금리와 유동성 지표 (2) | 2025.06.29 |

| [매크로] Stress DSR - To control the housing mortgage debt (0) | 2025.05.22 |

| [FICC] Korean Paper(외화채권) (1) | 2025.05.22 |